On the counter-cyclic evolution of VC funding in emerging markets

The end of 2017 brought a lot of debate about the “global implosion of the early-stage VC funding”. It all started with Victor Basta’s article in Techcrunch, addressed by Fred Wilson on his blog and soon shared by everybody all over the internet.

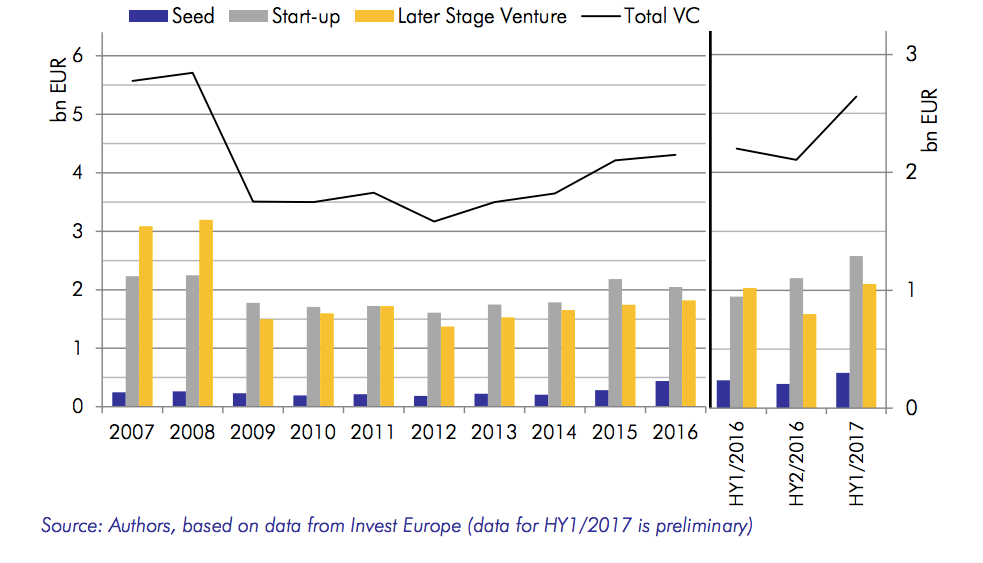

As proven by data, the fall in financing is indeed sharp. Both the number of deals and the value of investments have almost halved since 2014, marking the end of a fortunate period for early-stage startups raising money. But this is true only for the developed countries. The crash of the early-stage VC investment is anything but “global”.

In the emerging markets, especially in the countries of the New Europe, the crush of the early-stage VC funding never happened. On the contrary, VC investment is just taking off here.

Starting with 2018, new funds will be established in Romania, Bulgaria, Czech Republic, Greece, the Baltics and other countries in the Central and Southern Europe. With the likes of EIF as anchor LPs, the newly established VC firms will fill a major gap in the local ecosystems and will contribute to reducing the sizable differences in the development of the fragmented European VC markets.

This is part of a larger EU strategy according to which government agencies are to help the markets in a counter-cyclic way and increase their share in VC and PE firms. The effects of the public policy are already visible. In the first half-year of 2017, all VC stages contributed to the surge in investments on the continent: later stage VC +32% compared to HY2/2016; start-up stage +17%, seed stage +46%.

The expected result is a growing number of hot startups that will have access to professional investments for the first time, as recently proved by UiPath’s rising to be the darling of the European tech scene with a $30 mil Series A from Accel Partners and a strategic partnership with Oracle.

The average size of the early-stage VC fund in Europe is quite low (€49 mil in 2017) and the newcomers will be even below this threshold. In order to ensure significant returns, the new firms will be forced to scout for and invest in emerging business models and edge technologies. And this works perfectly for the local hordes of developers, currently employed by outsourcing companies or tech giants, who will be able to fully dedicate to their side projects in the blockchain, AI, RPA and other deep techs.

Saving the best for last, the public support and incentives greatly increase the prospective returns for private co-investors in the new funds. Hence the very appealing terms offered by EIF-backed fund managers.

The asymmetric distribution of proceeds in favor of the private co-investors is probably the most convincing (and quantifiable) argument.

While the early-stage VC crisis is ravaging in the US and Western Europe, the rise of new investment firms, run mostly by first-time fund managers, signals the dawn of a new era of opportunities in the East.